Did you know that global e-commerce sales reached over $4.1 trillion in 2024?

Every time someone makes a purchase, whether online or in a store, a payment system works behind the scenes to make it happen.

As a business owner, understanding how these systems work can help you avoid costly mistakes and keep your operations running smoothly.

When payments fail or take too long, it can frustrate your customers and sabotage your revenue. But it doesn’t have to be this way.

In this guide, you’ll learn how payment system works step by step, giving you the tools to make better choices for your business.

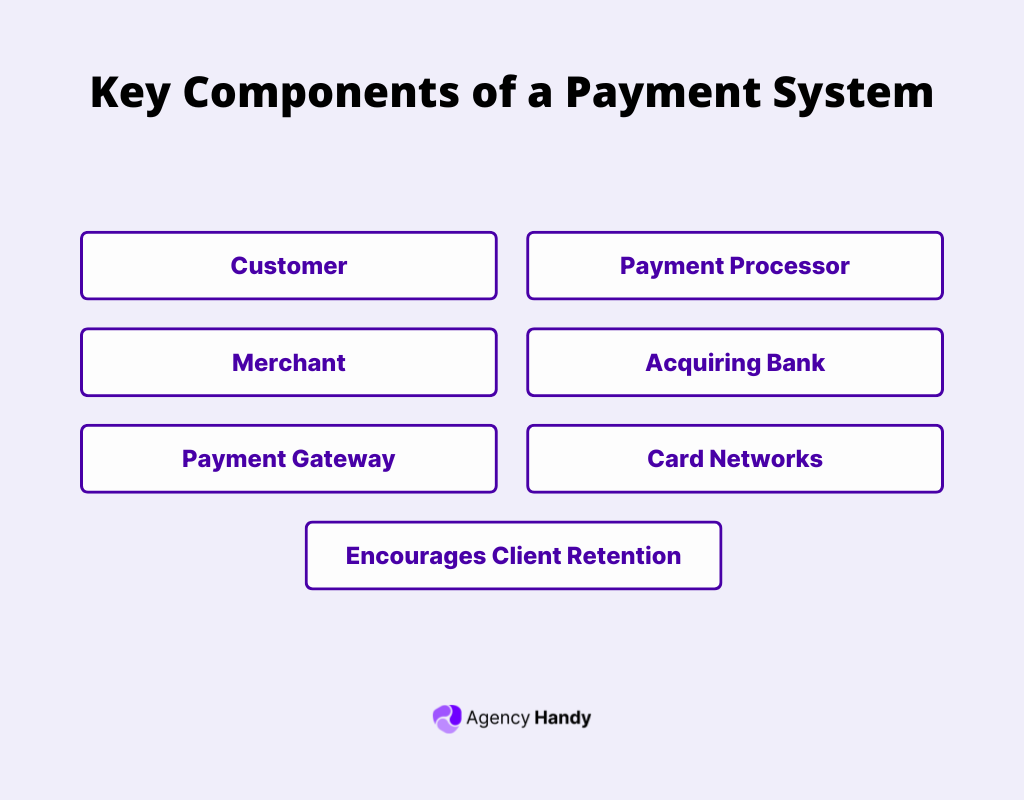

Key Components of A Payment System

Every payment system has several essential parts that work together to process transactions. These components ensure that payments are secure, fast, and reliable for both you and your customers. They are:

- Customer: The person or business making the payment.

- Merchant: You, the business owner, who is receiving the payment for goods or services.

- Payment Gateway: A tool that encrypts and securely sends payment details to the processor.

- Payment Processor: The system that manages the technical side of the transaction between the bank and card networks.

- Issuing Bank: The customer’s bank that approves or declines the transaction.

- Acquiring Bank: Your bank, which receives the funds after the payment is approved.

- Card Networks: Systems like Visa or Mastercard that connect the issuing and acquiring banks.

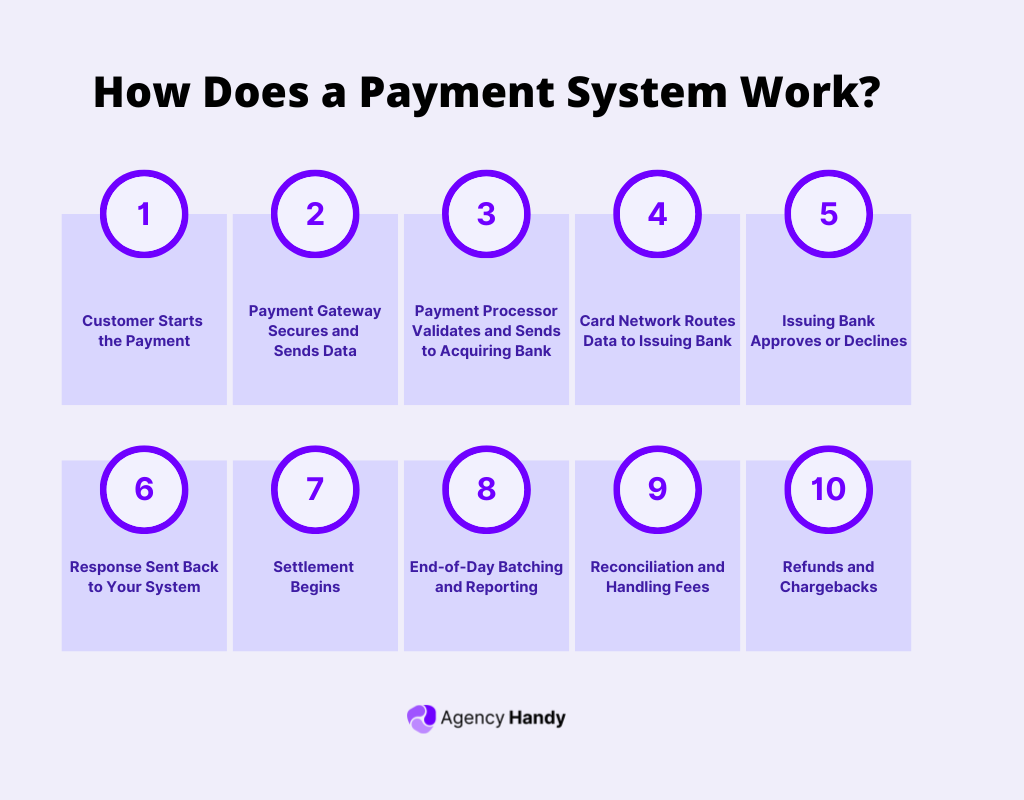

How Does a Payment System Work? A Step-by-Step Guide

When a customer makes a payment, a complex process takes place behind the scenes. Every step ensures the transaction is secure, accurate, and fast. Here’s how it all works.

Step 1: Customer Starts the Payment

The entire process begins when the customer enters their payment details. This could be a credit card, debit card, bank account, or digital wallet. Payments happen online, through apps, or at a physical checkout.

The details must be entered correctly. Even a small mistake, like a wrong card number or an expired date, can cause the payment to fail.

Step 2: Payment Gateway Secures and Sends Data

Once the customer submits their payment, the payment gateway encrypts the data to keep it safe. Encryption protects sensitive details like card numbers from being exposed.

The gateway then sends this encrypted data to the payment processor. It acts as a bridge between your system and the banking network, ensuring secure and smooth transactions.

Step 3: Payment Processor Validates and Sends to Acquiring Bank

The payment processor receives the data and quickly checks for errors or fraud risks. It verifies details like the card format and expiration date.

Once everything is confirmed, the processor forwards the request to the acquiring bank, which handles payments for your business.

Step 4: Card Network Routes Data to Issuing Bank

Once your acquiring bank receives the payment request, it sends it to the card network, like Visa or Mastercard.

The card network then forwards it to the customer’s bank, also known as the issuing bank.

This step adds an extra layer of security. The card network checks for fraud risks and ensures the transaction follows global payment standards.

If everything looks good, the request moves forward to the next step.

Step 5: Issuing Bank Approves or Declines

The issuing bank reviews the payment request and performs several checks:

- Is there enough balance or credit available?

- Are the card details correct and valid?

- Does the transaction look suspicious?

If the transaction passes all checks, the bank approves it. Otherwise, it is declined

Step 6: Response Sent Back to Your System

The bank’s decision (approval or decline) is sent back through the same channels: card network → acquiring bank → payment processor → payment gateway. Finally, your payment system receives the result.

This step happens almost instantly, ensuring a smooth experience for both you and your customers.

Step 7: Settlement Begins

If the payment is approved, the acquiring bank starts the settlement process. This means transferring funds from the customer’s bank to your business account.

Processing fees are deducted at this stage, and most transactions settle within one to three business days. Some providers offer faster payouts for quicker access to funds..

Step 8: End-of-Day Batching and Reporting

At the end of the day, all approved payments are grouped into a batch and sent to the acquiring bank. This process simplifies handling multiple transactions and lowers costs.

You also receive detailed reports summarizing daily sales, making it easy to track income and spot any errors.

Step 9: Reconciliation and Handling Fees

Reconciliation involves matching your sales records with the payments received in your account. This ensures that all transactions are accounted for and that no errors occur during processing.

It’s also during this step that you account for any fees charged by the processor, card networks, or banks. Automating this process can save time and improve accuracy.

Step 10: Optional Steps: Refunds and Chargebacks

Refunds and chargebacks are rare but important parts of the process.

- Refunds happen when you return money for a canceled order or returned product.

- Chargebacks occur when a customer disputes a charge, and the bank temporarily reverses the payment while investigating the claim.

To minimize disputes, have a clear refund policy and responsive customer support. Handling refunds efficiently builds trust and keeps customers satisfied.

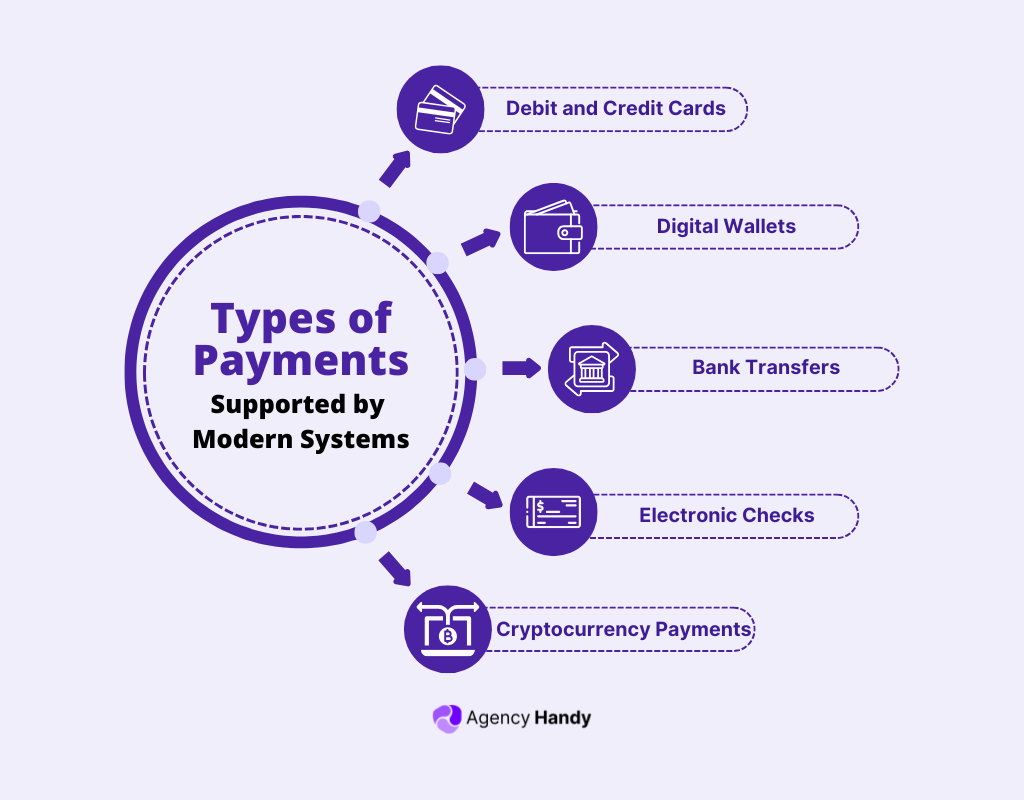

Types of Payments Supported by Modern Systems

Payment systems today allow you to accept a variety of payment methods, ensuring your customers can pay how they prefer while keeping transactions simple and secure.

1. Debit and Credit Cards

Debit and credit cards are the most common ways people pay, whether online or in-store. These payments go through networks like Visa or Mastercard and let your customers pay quickly and securely.

2. Digital Wallets (e.g., Apple Pay, Google Pay)

Digital wallets let your customers store their payment details on their phones and pay with just a tap. This method is fast, secure, and perfect for those who prefer contactless payments.

3. Bank Transfers

Bank transfers allow customers to send money directly from their bank account to yours. This method is reliable for high-value transactions, and payment providers like PayPal or Wise make it simple to handle domestic and international transfers.

4. Electronic Checks (eChecks)

eChecks are the digital version of paper checks. They are processed electronically and are great for recurring payments like rent or utility bills, offering a simple and cost-effective solution.

5. Cryptocurrency Payments (Emerging Trend)

Cryptocurrencies like Bitcoin and Ethereum are becoming more popular as payment options. They use blockchain technology to ensure secure transactions and work well for cross-border payments.

Conclusion

Understanding how a payment system works helps you offer smooth and secure transactions.

When you provide multiple payment options—credit cards, digital wallets, and bank transfers—you make it easier for customers to pay the way they prefer. This improves their experience and keeps your business running efficiently.

Choosing the right payment system simplifies billing, reduces errors, and helps you manage subscriptions or split payments with ease. Take the time to find a solution that fits your needs and keeps your transactions hassle-free.

FAQs

Are digital wallets secure?

Yes, digital wallets like Apple Pay and Google Pay use encryption and tokenization to keep payment data secure. These technologies ensure sensitive information is never exposed during transactions.

What are some payment processing examples?

Payment processing examples include swiping a card at a store, using digital wallets like Apple Pay, or transferring funds via PayPal. These systems securely transfer money between the buyer and the seller.

How can I reduce failed transactions?

To reduce failed transactions, ensure your payment forms are accurate and easy to use. Also, choose a payment processor with strong fraud detection and support for multiple payment methods to provide customers with alternatives.

How does the payment process in business work?

The payment process in business involves several steps: securing payment details, validating the transaction, routing it through banks, and settling the funds. Each step ensures the payment is completed accurately and securely.